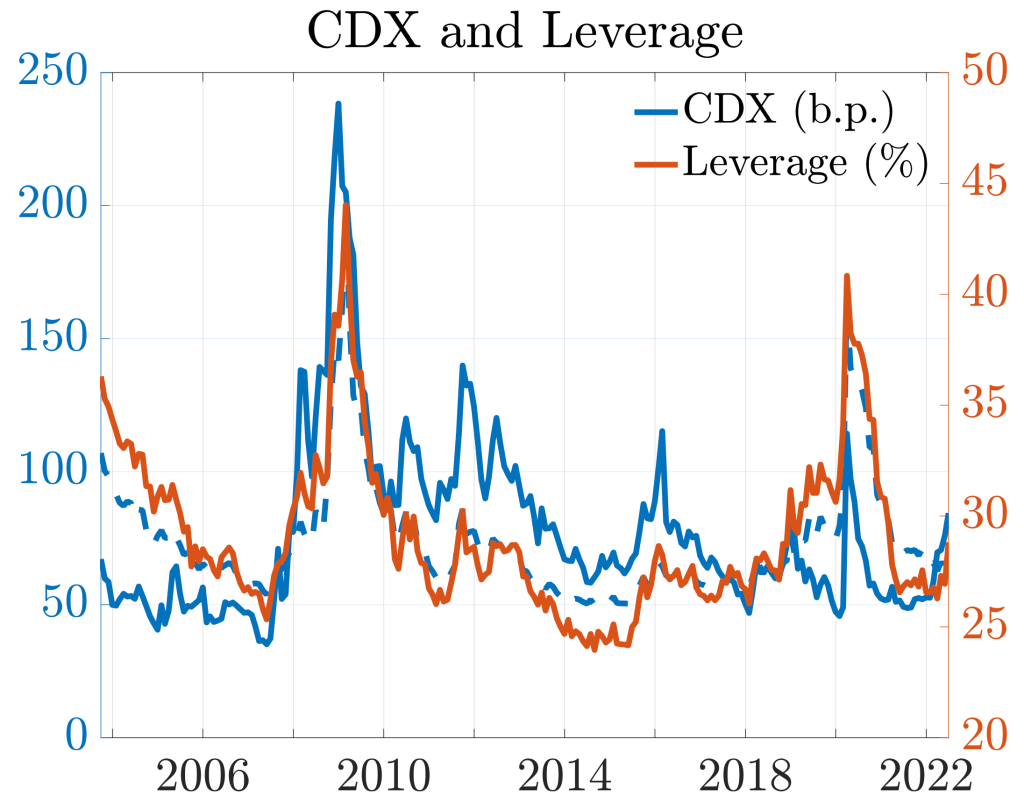

CDX spreads and corporate leverage comove strongly and more intensely during crises. Existing CDX pricing models cannot reproduce this pattern because they treat default and capital structure as exogenous. We develop a consumption-based model where firms optimally choose default and leverage while an Epstein–Zin representative agent learns about rare disaster risk. Rising disaster beliefs increase default boundaries and raise leverage, generating a fear-driven financing channel that elevates CDX spreads. We estimate the model to match the 5-year CDX rate, equity returns, and leverage. The model replicates the CDX term structure and physical default probabilities out of sample.